FIFO in plain terms

FIFO stands for first in, first out. The items you received first are the items you sell or use first. The oldest stock moves before the newest stock.

This applies in two different ways, and understanding both prevents confusion.

Physical FIFO: how you move goods

Physical FIFO means organizing your storage so older inventory is accessible and gets picked before newer inventory. When a new shipment arrives, it goes behind or below existing stock, not in front of it.

This matters most for perishable goods. A grocery store puts new milk behind old milk so customers grab the older cartons first. A bakery uses flour received last week before flour received today. A pharmacy dispenses medications with the nearest expiration date first.

Physical FIFO prevents spoilage and waste. Without it, older stock gets buried behind newer deliveries. It sits there past its useful life and becomes a loss.

Even for non-perishable goods, physical FIFO makes sense. Products can fade, packaging can deteriorate, and styles can go out of date. Moving older stock first minimizes these risks.

Cost FIFO: how you value inventory

Cost FIFO is an accounting method where the cost of your oldest inventory is matched against revenue first, regardless of which physical unit you actually shipped.

Example: You buy 100 widgets in January at $5 each and 100 widgets in March at $7 each. In April, you sell 50 widgets. Under FIFO accounting, you record the cost of those 50 widgets at $5 each (the January cost), even if you physically shipped widgets from the March batch.

This affects your cost of goods sold, your gross profit, and ultimately your taxes. When prices are rising, FIFO results in lower COGS and higher reported profits compared to LIFO.

Why FIFO is the most common method

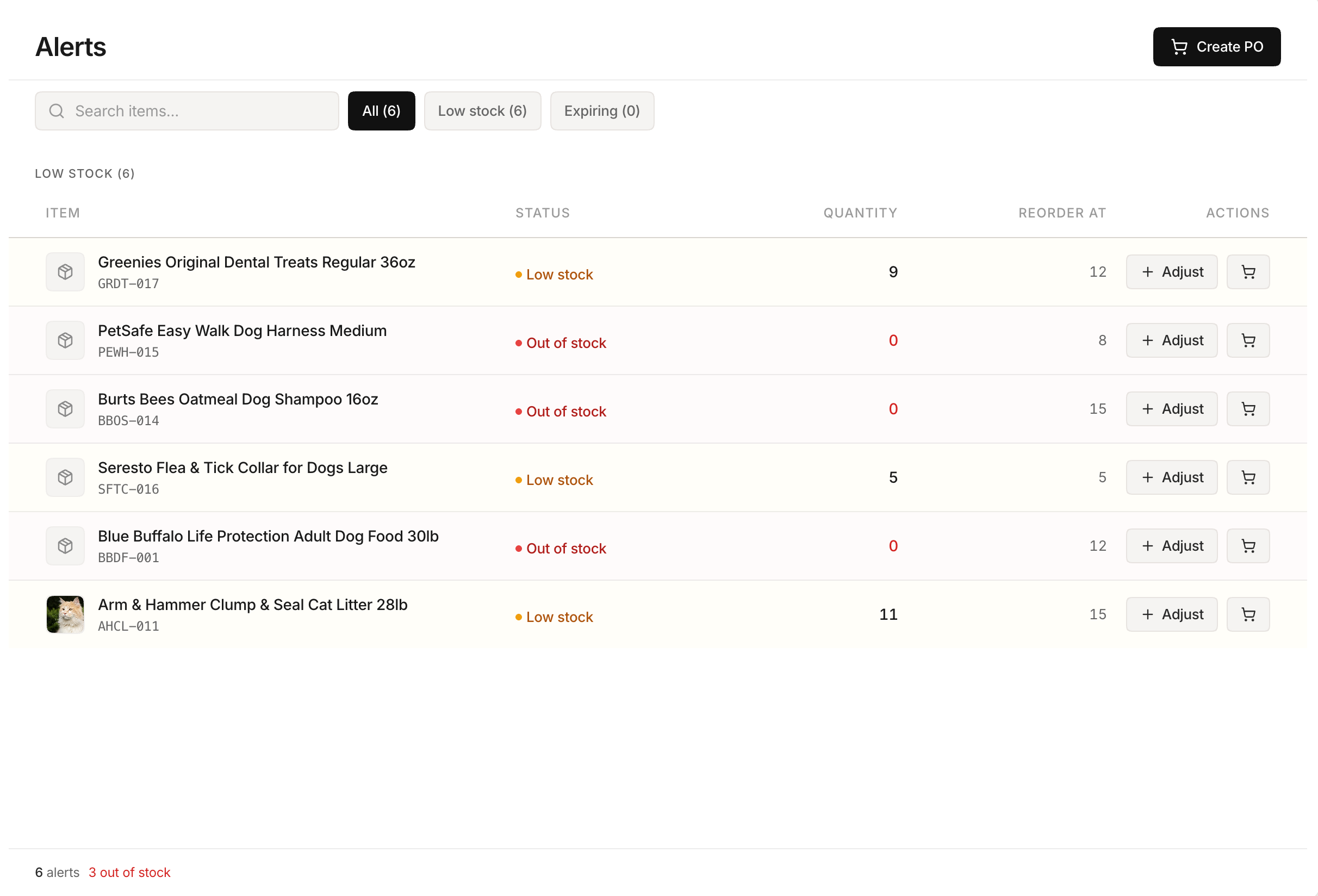

Stockria in action — Full alerts dashboard with days-until-stockout projections.

Stockria in action — Full alerts dashboard with days-until-stockout projections.

Most businesses use FIFO because it matches reality. In most operations, you naturally sell older stock before newer stock. The accounting method aligns with the physical flow.

FIFO is required under IFRS (International Financial Reporting Standards) and is the most common method under US GAAP. If you are not sure which method to use, FIFO is the safest default.

Your accountant or bookkeeper will likely recommend FIFO unless you have a specific reason to choose otherwise.

FIFO for perishable goods

If you sell food, beverages, flowers, cosmetics, pharmaceuticals, or any product with a shelf life, FIFO is not optional — it is essential.

Practical tips for maintaining FIFO with perishables: label everything with the date received, organize shelves so older items are in front, train every employee on FIFO stocking procedures, check dates during every receiving and stocking session, and set up alerts for items approaching expiration.

The cost of spoilage from poor rotation adds up quickly. A restaurant throwing away $500 in expired ingredients each month is losing $6,000 a year to a problem that discipline solves for free.

FIFO and your inventory software

Most inventory management software defaults to FIFO costing. When you sell an item, the system automatically assigns the cost of the oldest unit in stock. This happens in the background — you do not need to manually track which batch each sale comes from.

What software cannot do is enforce physical FIFO. That requires proper shelving, labeling, and staff training. The software handles the numbers; your processes handle the physical flow.

The bottom line

FIFO is both a physical practice and an accounting method. For perishable goods, it prevents waste. For accounting, it provides a clear and widely accepted way to value inventory and calculate profits. If you are just getting started, adopt FIFO for both and you will be on solid ground.